What is a stock?

A stock is not a ticker to trade. It is a piece of a business you own. Once you hold it that way, the price stops being the thing you watch and starts being the thing you exploit.

What is a stock?

A stock is a fractional ownership stake in a real business. It is a legal claim on a slice of the company’s equity: its assets after debts, and the residual value the business creates over time. Owning one share of a company with a hundred shares outstanding makes you the owner of one percent of its equity, with a claim on one percent of the economic value the business generates for its shareholders. What happens to those earnings, whether they are reinvested, paid out as dividends, or used to buy back shares, is decided by the board and management, not handed to you directly. The ticker that flickers on a screen is not the stock; it is the price the last buyer and seller agreed on for that ownership stake. The stock is the ownership. The price is just today’s quote on it.

This is the whole idea, and almost everything else in investing follows from taking it literally. In Invested, Phil and Danielle Town spend a book getting to one instinct: buy a stock the way you would buy the entire business, because that is what you are doing in miniature. Warren Buffett has made the same point for sixty years. He does not buy stocks, he buys businesses that happen to have shares for sale.

I am a better investor because I am a businessman, and a better businessman because I am an investor.

The practical test the Towns hand a beginner is the Four Ms: a business has to have Meaning (you understand it well enough to own it), a Moat (a durable advantage that protects its earnings), good Management, and it has to be available at a Margin of safety to what it is worth. Three of the four are about the business. Only the last is about the price. That ratio is the entire point: most of the work of owning a stock is understanding the company, not predicting the quote.

Why does a stock’s price matter to the company itself?

Daily trading happens between investors and sends the company no cash. When you buy a share of Apple, Apple gets nothing; the seller does. So it is tempting to think the price is irrelevant to the business. It is not, because the market price strongly influences the company’s cost of equity capital. When the stock is richly valued, the firm can raise a given sum of money by issuing fewer shares, which means each existing owner is diluted less per dollar raised. A high price lowers the cost of the most patient money a business can use.

It helps to separate two events. When a company first sells shares to the public, or issues new ones later, the cash goes to the company, and that is the moment a stock funds a business. Every trade after that is the secondary market: ownership changing hands between investors, with the company watching from the sidelines. The price set in that secondary market is what governs the terms on which the company can come back for more. A business whose shares trade at a high multiple of its earnings can raise a war chest by issuing a small sliver of itself; a business whose shares are cheap has to sell a large slice to raise the same money, diluting its existing owners far more. Price, in other words, is not just a scoreboard. It strongly influences the terms on which a company can raise equity, the most patient capital it will ever use.

How does a high stock price strengthen the balance sheet and borrowing power?

Equity is the cushion that sits beneath the debt on a balance sheet, and lenders care most about cash flow, assets, and debt coverage. A high market value does not directly increase the accounting equity recorded on the balance sheet, since that figure reflects capital raised and profits retained, not the share price. What a high valuation does improve is financial flexibility: it signals investor confidence, opens an additional source of capital, and strengthens the overall financial position a lender assesses. A richly valued stock is also a currency: management can buy another company by issuing its own shares rather than draining cash, and shares can be pledged as collateral.

Three concrete advantages flow from a strong share price. First, cheaper acquisitions: a company with a richly valued stock can buy a rival by handing over its own shares instead of cash, and when its currency is dear, it pays for the target with relatively little of itself. Second, borrowing power: a strong market value improves a company’s borrowing flexibility. It signals investor confidence and strengthens the overall financial picture, though lenders still decide primarily on cash flow, assets, and debt coverage. Shares themselves can also be posted as collateral. Third, resilience: a company that can raise equity cheaply when it needs to is far harder to push into a corner during a downturn. The flip side is the discipline this demands of you as an owner. Issuing shares when they are cheap, or buying back when they are expensive, destroys value, and watching which way management leans is one of the clearest reads you get on them. The balance sheet is where all of this shows up; reading it is its own skill, covered in the three-statements piece.

Why is investing in quality companies at a fair valuation less risky?

Because two different things have to go wrong before you lose money, and quality plus a fair price guards against both. Quality, meaning a durable competitive advantage earning high returns on capital, keeps the business compounding value whether or not the market is paying attention. A fair price means you are not relying on a re-rating to make the investment work; the margin of safety is the gap between what you pay and what the business is worth. The downside protection comes from the business, not from the mood of the next buyer.

Notice that this is the opposite of how risk is usually sold. The common story is that higher returns require higher risk, so the way to make more is to bet on more volatile, more speculative things. The value-investing answer is that the durable way to lower risk and raise return at the same time is to own a genuinely good business and refuse to overpay for it. A fair price on a fragile business still leaves you exposed to the business failing; a great business bought at a reckless price still leaves you exposed to years of waiting for the math to catch up to the multiple. You want both halves. The quality is what compounds; the price is what protects you while it does. The mechanics of the price half (what intrinsic value means and how to size the buffer) live in the margin-of-safety piece, and the mechanics of the quality half (moats, ROIC, and reinvestment) live in quality compounders. This article only needs you to hold both in mind at once.

How do buybacks and dividends lower an owner’s risk?

Both return cash to owners, the part of the return that does not depend on Mr. Market’s mood on the day you want it. A dividend reduces risk plainly: it is realised cash in your hand. A buyback is more conditional. It retires shares, so your slice of the business grows without you buying more, but it only rewards the remaining owners when shares are repurchased below intrinsic value, funded from surplus cash, and not at the expense of better reinvestment or a healthy balance sheet. Done on those terms it raises everyone’s stake in the business; done carelessly it destroys value, as many poorly timed buybacks have. Returned capital, used well, is the return you keep regardless of where the quote sits next quarter.

A business that earns more cash than it can sensibly reinvest has three honest things to do with the surplus: reinvest it at a high return, pay it out as a dividend, or buy back its own shares. The last two are how a stock pays you without your having to sell it. A dividend is the simplest: cash arriving on a schedule, a return that does not care what the quote does. A buyback is subtler and often misunderstood. By retiring shares, it shrinks the number of slices the business is divided into, so your slice grows. Phil Town frames a well-timed buyback as lowering your effective cost in the business, but it is worth being precise: your tax cost basis does not change. What rises is your ownership percentage, as the share count falls, and with it the intrinsic value per share of the stake you still hold, without your lifting a finger.

The discipline is everything. A buyback only creates value when the company repurchases below what the business is worth; buying back overvalued stock burns the owners’ cash to flatter a per-share number. The same judgement that tells you whether to buy the stock tells you whether management should be buying it too. Capital allocation read this way (reinvest, pay out, or repurchase, and at what prices) is the clearest window onto whether the people running your business think like owners, the theme of the evolution-of-value-investing piece.

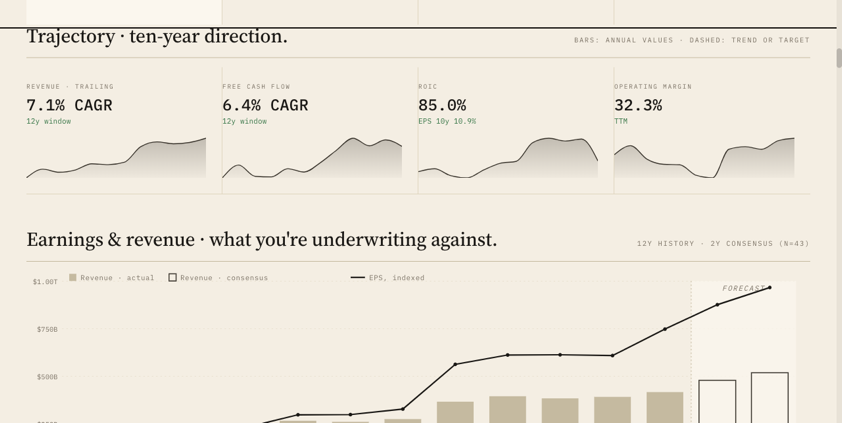

How do I evaluate a stock as an owner in Invest Board?

Treat the share as the business it represents and work the two surfaces together. The Discover screener narrows the universe to durable, high-return businesses trading at sensible prices. The Company page then lets you underwrite one as an owner: the Understand tab scores the moat and management, and the Value tab reads ROIC, free cash flow, and the trajectory of the business across years. The point of the workbench is to make you think like a part-owner, not a ticker-watcher.

The product is built around the one shift this article is asking you to make: stop watching the ticker and start underwriting the business. The Discover screener filters the universe down to durable, high-return companies available at sensible prices, the Four-Ms shortlist made mechanical. From there, a Company page is the owner’s desk: the Understand tab scores the moat and the quality of management, the Value tab reads return on capital and the multi-year trajectory of revenue and free cash flow, and the Decide tab is where you write the conditions that would make you sell. None of it predicts next week’s price. All of it helps you answer the only question an owner actually has: is this a good business, and is this a fair price to own it? The fuller version of that checklist, and the thinking behind every score, is on the Process page.