Quality compounders

Strong margins attract competition. The moat is what keeps the margins from being competed away. The math runs on ROIC, the patience runs on conviction, and the premium the market pays is the entry tax for the holding period that lets the math run.

What is a quality compounder?

A quality compounder is a business whose returns on invested capital are durably high, that can reinvest the cash it earns back into the same or adjacent opportunities at those high returns, and whose moat is structural rather than stylistic. The combination matters. High ROIC alone is a snapshot; high ROIC plus reinvestment runway is geometric compounding; and the durable moat is what keeps competitors from competing the returns away long enough for the geometry to do its work.

The single most important decision in evaluating a business is pricing power. […] The key to investing is determining the durability of the competitive advantage.

Buffett's framing is the formulation every later definition of the category is built on. The headline number is ROIC. The underwriting work is the moat.

Why is ROIC the headline number for compounder investing?

Because the long-run equity return of a reinvesting business converges on ROIC times the reinvestment rate. That relationship dominates entry multiple, sector tailwind, and even management quality over long horizons. ROIC is the cleanest single measure of capital efficiency, and the business whose ROIC is high and durable is the business whose equity actually compounds. Buffett's emphasis on return on capital across the Berkshire letters is for precisely this reason.

The arithmetic is mechanical and worth pausing on. The long-run return of a non-growing business converges on its return on invested capital: if all the cash is paid out as dividends, the equity return is the ROIC. The long-run return of a reinvesting business compounds at roughly ROIC times the reinvestment rate. A business earning 25% on capital and reinvesting half of what it earns will compound book value at approximately 12.5% a year before any multiple revision; one earning 8% and reinvesting half compounds at 4%. Over a twenty-year holding period the math separates the two by a factor of four on the equity alone — before the market revises its view of which business is which.

The Process page's framing is the canonical one for this product.

Over time a non-growing company will not generate more return than its ROIC. So if you can find companies with high ROIC that is also growing and reinvesting its earnings at high ROIC, it will generate a lot of wealth for you. Strong moat is required to keep the competition at bay.

Growth is the runway

The ROIC math assumes the business can keep redeploying capital at the headline rate. That assumption is doing a lot of work. The reinvestment rate is bounded by the opportunity set: how much capital the business can put back to work at the same return. A 25% ROIC business in a saturated market with no place to redeploy is, in the limit, a payout business: the long-run equity return reverts toward the dividend yield, not the ROIC. A 25% ROIC business with a long runway of adjacent expansion opportunities (new geographies, new product lines, new customer segments where the same competitive advantage transfers) is the business that actually compounds at the headline rate. Top-line growth is the receipt that the reinvestment rate is real.

The qualitative read for this is the same instinct as the moat work, applied forward instead of backward: where can the next dollar earn the same return as the last one? The moat tells you whether the existing business will keep its returns; the reinvestment-opportunity read tells you whether the next business (the geography, the adjacency, the new line) will earn them too. Inside Invest Board, the AI-derived achievable growth rate on the Value tab is the product's read on the opportunity-set durability; the Moat pillar on the Understand tab is the read on whether the moat travels into that runway. The compounder thesis sits across both.

What kinds of moats actually keep margins high?

Strong margins are the magnet that attracts competition — returns above the cost of capital invite capital. The moat is the wall that keeps rivals out long enough that the compounding math runs uninterrupted, and a handful of categories recur across the businesses that hold: network effects, brand, switching costs, cost advantages, regulatory protection, proprietary technology, economies of scale, and irreplaceable physical assets.

- Network effects. Facebook and Google get more valuable as more users join the platform: the value to each additional participant compounds with the size of the network.

- Brand. Apple and Coca-Cola command premium prices and customer loyalty that survive every macro cycle and every product transition.

- Switching costs. Microsoft and Adobe make it expensive (in workflow, training, and integration) for customers to leave.

- Cost advantages. Amazon and Walmart pass scale and process efficiency into prices that smaller competitors cannot match.

- Regulatory protection. Visa and Mastercard sit behind regulatory barriers so high that new entrants cannot replicate the rails.

- Proprietary technology. Innovations that competitors cannot easily replicate, protected by patents, process knowledge, or sheer engineering depth.

- Economies of scale. Fixed costs spread across volume that smaller competitors cannot match without years of capital and execution.

- Irreplaceable physical assets. Railroads, airports, pipelines, port concessions — infrastructure that simply cannot be rebuilt by a new entrant.

Investor Chris Horn calls the durable moat the single most important factor in his investment decisions. Terry Smith goes the inverse route and avoids entire sectors he believes structurally lack moats: banks, manufacturers, airlines, transportation, mining. Both arrive at the same place: the moat is not a feature you check; it is the precondition for the rest of the analysis to be worth doing.

Why do quality compounders trade at higher P/E ratios?

Because the market is paying in advance for a holding period the compounding math actually rewards. A higher ROIC × reinvestment rate means equity compounds faster, and the multiple gap closes over time as the business outgrows the discount. The premium is the entry tax for the holding period that lets the math run.

A great business at a fair price is superior to a fair business at a great price.

Munger's famous lesson is the insight Buffett credits with shifting him from a Graham-style cigar-butt investor into the Berkshire compounder he became. Phil Fisher's fifteen-point checklist in Common Stocks and Uncommon Profits is the empirical neighbour: profit margins, management's attitude toward shareholders, R&D effectiveness, depth of the management team, product cycle, sales organisation. None of the fifteen test the multiple. All of them test the durability that justifies one.

When does the compounder premium become a value trap?

When ROIC starts compressing and the moat starts looking less durable than the multiple assumes. The same math runs both ways: if returns on capital fall from 25% to 15%, the multiple compresses faster than the earnings, because the market re-rates the duration of the moat, not just the level. A compounder bought at 35× P/E that compounds at 6% instead of 12% does not return capital quickly; it returns it eventually, but the IRR collapses.

The classic break patterns sit in the same categories that built the moat: a competitor entering an adjacent niche, regulation reshaping the cost structure, network effects fragmenting as users migrate to a new platform, brand fading with a generational shift, switching costs eroding as a vendor-neutral standard emerges. The discipline that protects against this is the moat re-underwrite, done annually and on every material print. The companion red-flag screen lives on the value-trap checklist.

There is a duration mechanic that compounder investors should hold in mind alongside the moat work. When rates rise, long-duration cash flows compress harder than near-term ones, and compounders — almost by definition long-duration — feel the re-rating first. The fix is not to fight the rate cycle; it is to make sure the moat is intact enough that the cash flows in years ten through twenty actually arrive. The investment clock post carries the macro framing.

How do I find quality compounders in Invest Board?

Two surfaces work together. The Discover page's screener filters the universe down to high-ROIC names with durable moats and reinvestment runway: set the lens to Value, screen on ROIC, moat strength, and the AI achievable growth rate. Then drill into a Company page: the Understand tab's Moat pillar answers will it keep compounding; the Value tab's Trajectory strip answers has it actually compounded. Together they're the workbench.

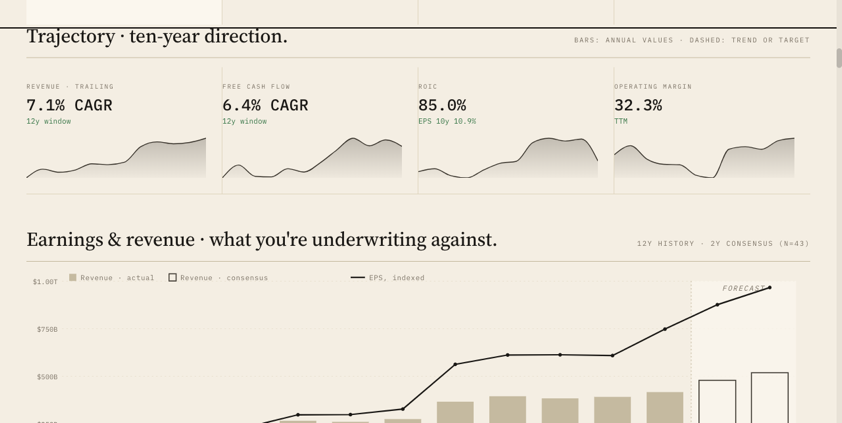

The screen's result is the working set: the candidates that pass the structural test before you do any bottom-up underwriting. On the Company page, the Moat pillar scores each moat type (network, brand, switching, cost, regulatory, IP, scale, irreplaceable assets) with strength and rationale, surfacing the AI's read of where the durability actually lives. The Trajectory strip (shown above) reads revenue, free cash flow, ROIC, and operating margin across twelve years with sparklines beneath each headline number: the empirical receipt for whether the business has historically compounded. The Decide tab's kill criteria editor is where you write the moat-erosion conditions that would force you to exit: the underwriting that turns a compounder thesis from a story into a falsifiable claim.

The patience side

Compounders pay the patient. Buffett's most-quoted lines on the category are not about the buying; they are about the holding.

Time is the friend of the wonderful company, the enemy of the mediocre. […] Our favourite holding period is forever.

Phil Fisher's framing in Common Stocks and Uncommon Profits is the same instinct.

If the job has been correctly done when a common stock is purchased, the time to sell it is — almost never.

The lines are quoted enough that they read as cliché; the mathematical fact behind them is anything but. Holding a quality compounder at 12% for thirty years is a 30× on the equity — exiting at year five for a 50% gain gives up an order of magnitude to lock in a single year's worth of index return.

Gautam Baid devotes the spine of The Joys of Compounding to the same arithmetic from the personal-capital side: small, consistent compounding at high rates is what builds the wealth, not the occasional ten-bagger and certainly not the trading record. The discipline that lets you actually be patient with a compounder is the moat work done at entry: when the next quarter looks soft and the multiple compresses, the moat re-read is what tells you whether the thesis is broken or just being tested. Patience compounds because the underwriting is honest, not the other way around.