This is a tool I built because the one I wanted didn't exist.

Most investment software is built for traders: dashboards full of blinking numbers, short-term signals, and noise. I wanted something built on a different premise: that investing is fundamentally an intellectual act. Read the business first. Understand the moat. Judge the management. Only then count the numbers.

Value investing, at its core, is about following your principles regardless of what the crowd is doing. That requires a certain kind of freedom: the freedom to be wrong for a year and not care, to hold when others are selling, to pass on things that feel exciting but fail your written criteria. Money makes that freedom possible. It is not the end; it is what keeps you in the game long enough for the good decisions to compound.

The hardest part of this is not the analysis. It is the psychology. Greed when a position runs past your price target. Fear when it falls and the thesis feels uncertain. Impatience when nothing is moving and cash is sitting idle. Every mistake I have made in twenty years came from one of those three. investboard exists to support the process that holds them in check: a written thesis, a kill criterion set in advance, a briefing that speaks only when something has actually changed against your own criteria. The discipline does not come from willpower. It comes from having done the work beforehand and written it down.

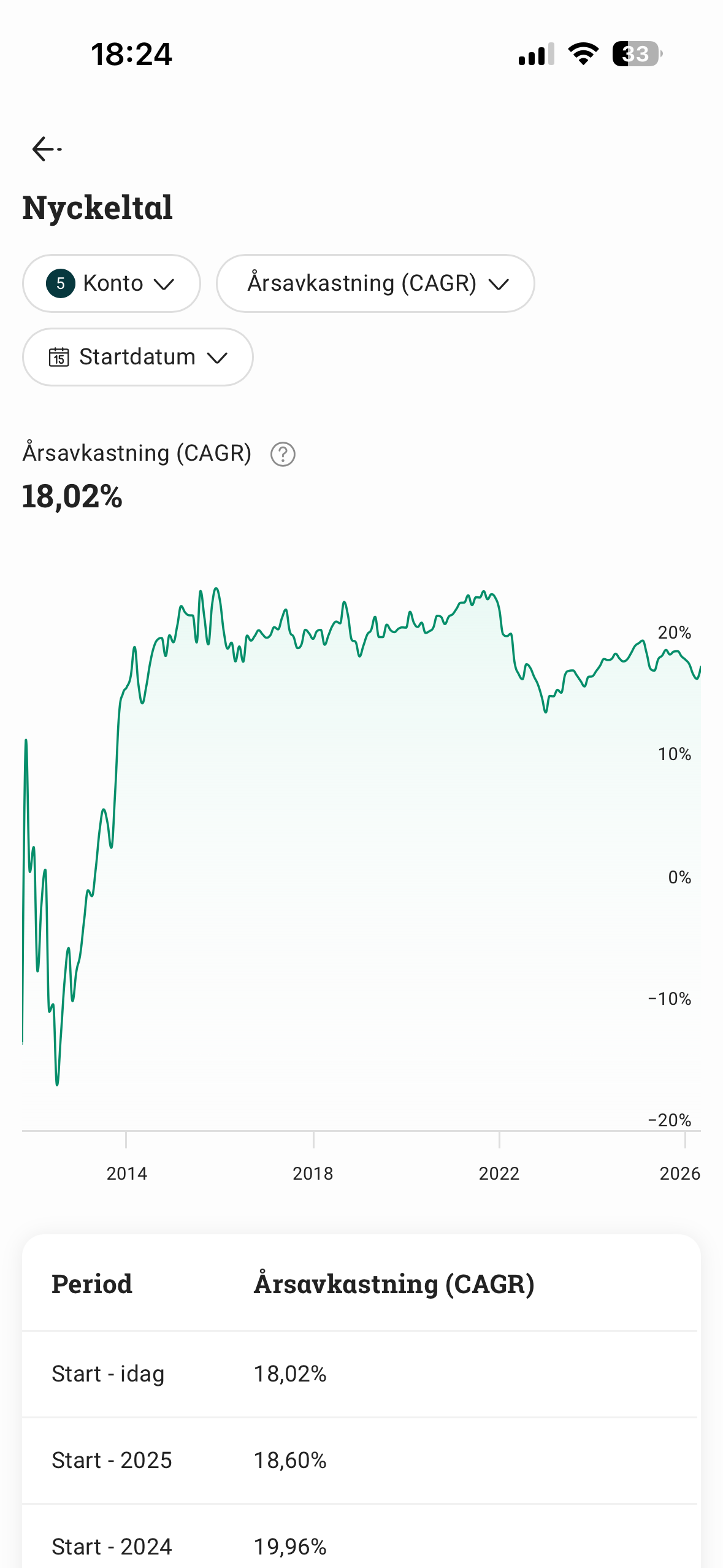

I have run my own book for over twenty years, compounding at roughly eighteen percent a year. The work I enjoy most is the reading (annual reports, letters, histories of industries and companies) and sharing what I find with people who find it equally interesting.

The process you will find in this product is not original. It is cloned, deliberately, from investors who have proven it works over decades. Graham's margin of safety. Buffett's moat framework. Munger's mental models and inversion. Pabrai's checklist discipline. Lynch's business common sense. Druckenmiller's forward-looking conviction. Cloning the best is itself a principle: why reinvent a method that Buffett has compounded at twenty percent for sixty years? The only contribution here is the tool that makes it easier to apply consistently.

If you read fund letters more than you read Twitter, if you have written down a kill criterion and lived by it, if you would rather wait three years for the right setup than chase ten wrong ones — this was built for you.

The author behind the briefing.

Magnus has spent twenty years running a concentrated personal book of fundamentally underwritten businesses. The portfolio compounds at roughly eighteen percent a year, verified through his Avanza Bank brokerage account. The methodology is qualitative first (moat, management, culture), then quantitative: margin of safety, normalised earnings, valuation gap. The analysis serves the thesis, not the other way around.

He builds investboard for the same reason he invests: because the work itself is worth doing. The reading, the pattern recognition, the intellectual delight of watching a thesis play out over years. Every feature exists because Magnus needed it, used it, refined it, and shipped it, first to himself, now to you.

Below: snapshots from the actual brokerage account. Numbers are real; ticker-level positions are not disclosed.

Source: Avanza Bank (Sweden). Numbers are real; redacted for the public web.

Six principles, the rest is plumbing.

- 01

Qualitative first. Quantitative always.

We read the filing before we run the model. Understanding the business (its competitive position, its culture, the quality of its management) is the primary analysis. The margin of safety calculation is its conclusion, not its beginning. Numbers are precise; insight is prior.

- 02

A few great ideas, held with conviction.

The goal is not to own thirty businesses you half-understand, but three you know deeply. Every major insight in investing comes from spending more time than others on fewer things. Breadth is a symptom of uncertainty. Concentration is the reward for clarity.

- 03

Process over prediction.

We do not forecast markets, score sentiment, or sell signals. The product is a repeatable underwriting process (moat, management, margin of safety) applied identically to every company you research. Discipline travels; predictions don't.

- 04

Idea first. No screening.

Start from a narrative, a misunderstanding by consensus. Then ask whether it can be mispriced, not the other way around. Screeners find cheap stocks; they do not find great businesses underappreciated by the market. The insight comes first, the valuation is its test.

- 05

Value investing is forward-looking.

One hundred percent of the information you have about any business reflects the past. One hundred percent of its value depends on the future. We do not project the recent past into the future; we visualise where the business will be in ten years and ask whether today's price accounts for it. The job is to find futures that are not yet in the price.

- 06

Freedom is the real return.

The number in the portfolio is not the goal. The goal is independence: the freedom to do work that matters to you, live by your own calendar, and say no to things that waste your one life. Seneca wrote that life is long if you know how to use it. Compounding is how investors use it.

The omissions are the product.

Every absence below is a design decision, not a backlog item.

- —

No push notifications.

A briefing arrives once after the close. If you need to be interrupted to manage a portfolio, the portfolio is not built for compounding.

- —

No intraday ticker tape.

No candles, no heatmaps, no "your portfolio is up 0.3%" widget. Daily prices are noise; the briefing speaks only when something has actually changed against your written discipline.

- —

No homepage feed of trending stocks.

Crowds are a leading indicator of bad ideas at high prices. We will not put a "what's hot" panel in front of an investor on their way to underwrite a business.

- —

No auto-trading. No managed money.

The decision belongs to you. We will never insert ourselves between an investor and their broker.

"Omnia, Lucili, aliena sunt, tempus tantum nostrum est." Everything is alien to us, Lucilius — time alone is ours.

Seneca · Epistulae Morales, IWhere every number on every page comes from.

10-K, 10-Q, 8-K annual and quarterly filings

SEC EDGARIncome statements, balance sheets, cash-flow statements

EDGAR · normalisedReal-time market pricing and historical data

Exchange directAnalyst consensus estimates and forward projections

AggregatedInsider transaction filings and institutional holdings

Form 4 · 13G/DSuper-investor portfolios (Buffett, Ackman, Klarman, Pabrai, more)

13F quarterly

Magnus reads every message personally. Reply within forty-eight hours on weekdays, longer if the markets are doing something interesting.

Set in Source Serif 4 and IBM Plex. Quiet by design.

This is not investment advice. investboard is an informational and analytical tool only. Nothing on this platform constitutes a recommendation to buy, sell, or hold any security. Always do your own research and consult a qualified financial adviser before making investment decisions.