Investment Journaling for Value Investors

Memory rewrites the thesis to match the price. The journal is what holds the original claim still long enough for past-you and future-you to disagree.

What is an investment journal and why do value investors keep one?

An investment journal is a written record of every position decision (entry, hold, trim, sell) together with the thesis that produced it and the emotional state you were in when you made it. Value investors keep one because the discipline depends on something the brain is not reliable at: comparing what you actually believed at entry to what you are defending in your head today. Memory is a liar. Memory rewrites the thesis to match the price. The journal is the only mechanism that lets past-you and future-you have an honest conversation about whether the work you did still holds.

Buffett does not keep a public journal, but the annual letters function as one: the same business reviewed across the same dimensions year after year, the same vocabulary, the same restraint. Klarman has written that the discipline of writing a thesis down at entry is what separates investors who learn from their mistakes from investors who merely repeat them with different tickers. The mechanism is the same in both cases: a written claim is a contract with future-you, and the contract is what lets the discipline survive the next stretch of weeks when the price is doing the work of feeling like a refutation.

Gautam Baid devotes a chapter to journaling in The Joys of Compounding, and his framing is the one this playbook is built on: the journal is not a record of what you bought but a record of what you believed when you bought it. Baid argues, citing Munger, Kahneman, and Annie Duke, that the outcome-versus-process distinction is the single most useful one in investing, and that the journal is the only mechanism that lets you grade process independently of outcome. Two years from now, the price will have told its own story. The journal entry is the only place that records whether the story matches the work.

What should go in a single journal entry?

Three things, in this order. First, the claim: one or two sentences stating what you believe the business will do that the market currently does not. Second, the kill criterion: the specific, falsifiable condition that would tell you the claim is wrong (gross margin below X for two quarters, churn above Y, debt-to-FCF above Z). Third, the edge note: why now, what advantage you have, what you are paying for that the market is not. Everything else is decoration. An entry without those three things is a trade log, not a journal.

The temptation when you write a thesis is to write the version that sounds defensible to the analyst inside your head. That version is almost always too long and too hedged. Pabrai's discipline is the opposite: if you cannot state the thesis in two sentences, you do not yet have the thesis. The two-sentence form forces the claim to be about this business and not the sector, not the macro backdrop, not the market regime. The macro framing can live in the body of the entry. The two-sentence claim is the part that has to survive being read aloud to a sceptic.

When should you journal? Every trade, or only the big ones?

Every trade, but with different depth. Every buy and every sell gets a full entry. Every thesis check (quarterly is plenty for stable positions) gets a short entry: usually one paragraph confirming the kill criteria are intact or naming the ones that have moved toward the line. Earnings prints that materially confirm or break the thesis get an entry. Watchlist updates (adds, removes, why-now changes) get an entry. The watchlist names you almost bought and did not get an entry too, because that is where the discipline against FOMO lives. Six months later, half of those almost-bought names will look terrible, and remembering that is what protects future you from the next one.

The watchlist entries are the underrated half of the journal. Most investors keep good records of what they bought. Very few keep records of what they almost bought and chose not to. That asymmetry is the reason FOMO is such a durable bias: there is no record of the almost-bought name that fell forty percent six months later, so the next almost-bought name feels like the one you cannot afford to miss. A two-line entry is the cheapest insurance against repeating the pattern: "Considered MOMENTUM-NAME at $X on Y date; did not buy because Z". Read those entries six months on; most of them age into validation of the original restraint.

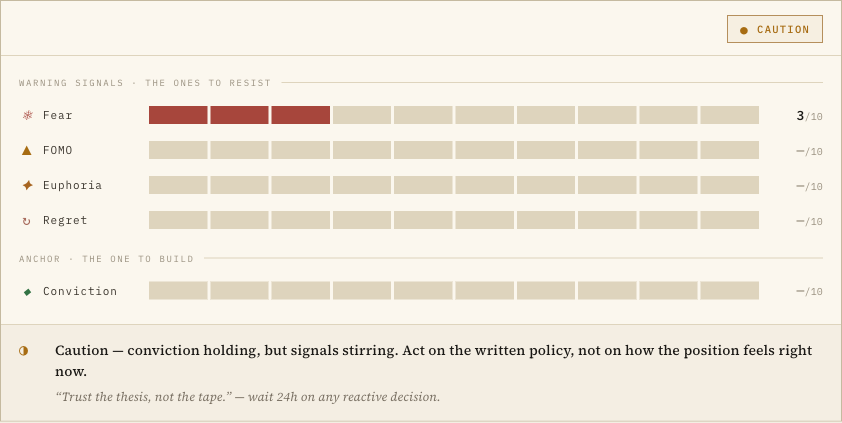

How do you log psychology without it becoming theatre?

You rate yourself on five axes (Fear, FOMO, Euphoria, Regret, Conviction), each on a zero-to-ten scale, and you do it before the decision rather than after. The four warning emotions are the ones to notice and resist; conviction is the only one to cultivate. The honest test is whether the rating you put down today would survive a sceptical reading by past-you. If you find yourself routinely landing on "five out of ten" on everything, the journal has become theatre. The axes work when the readings are uncomfortable enough to be revealing. That usually means fear or euphoria touching seven or above.

The taxonomy the Invest Board journal uses comes from the value-investing literature directly: Buffett's be greedy when others are fearfulnames Fear; Klarman's repeated warnings against speculation name Euphoria and FOMO; Munger's invocation of sit on your handsnames Regret as the anchor that makes past mistakes contaminate present decisions. Conviction, the only positive axis, is the one Buffett describes as the willingness to sit there while the market does what it does. Each axis is independent. A high Conviction reading with a high Fear reading is exactly the disciplined entry the framework rewards. A high FOMO reading with a high Conviction reading is the entry that should not be executed today — there is a 24-hour rule for a reason.

How do you review the journal so it actually pays back?

Three review cadences. Weekly: scan the entries you made in the last seven days. Did any prediction resolve? Was it correct? Quarterly: open each owned position's entries, side by side with the current price, and ask whether the thesis at entry is the thesis you would write today. Where they diverge, you have an anchor or a confirmation bias at work. Annually, in a fixed week (many investors pick the week between Christmas and New Year), re-underwrite every position as if it were a fresh buy. The positions that survive are the ones you actually believe in. The ones that fail were being carried by the anchor of the entry price, not the work.

The annual re-underwriting cycle is where the journal earns its keep. Pick the week. Open every position's entry. Read it. Compare the thesis as written to the thesis as it would be written today. Some positions will have improved: the original claim was right, the business has compounded, the kill criteria stayed intact, the conviction-at-entry was justified. Most years, one or two positions will fail the test: the thesis written today does not look like the thesis written then, the kill criteria you would set today are tighter than the ones you wrote, the conviction-at-entry was rationalised. The act of selling those positions is almost always the highest-return decision of the year, and the journal is the only mechanism that produces it. Without the journal, those positions survive because the brain that holds them in the portfolio is not the brain that bought them.

What are the common journaling mistakes that make it useless?

Four. First, free-form prose with no falsifiable claim: the entry ages into a story instead of a test. Second, entries written after the price has moved, capturing the rationalisation rather than the reasoning. Third, no review cadence. Entries that get written and never re-read are a write-only journal, which is the same as no journal. Fourth, treating the journal as a confessional rather than a forecasting record: recording feelings without committing to a specific outcome that can later be marked confirmed or disconfirmed. The discipline only compounds when the same entry can be graded against reality six months later.

The most damaging mistake is the third one — the write-only journal. It costs you the discipline twice: once because you spent the time writing, and again because the time-stamped record of your past thinking is just sitting there unread, waiting to validate the revisionist version that lives in your head. The fix is the cadence, not the volume. A small journal reviewed weekly compounds. A beautiful journal opened once a year does not. The discipline of review is the discipline of the journal; everything else is the prerequisite.

What's the smallest journal that still works?

Two columns per position, kept in any text file or spreadsheet that opens fast. Left column: the dated entry (one sentence claim, one sentence kill criterion, one sentence edge). Right column: the resolution (what actually happened, marked confirmed or disconfirmed within twelve months). Add a third column for the psychology rating if you can keep yourself honest about it. The smallest version of any habit is the one that survives the busy week. A two-column file beats an elegant journal that requires forty minutes to write in.

For investors building the habit from scratch, the strongest recommendation is to start with the two-column file and add only the third column, psychology, once the first two are reliably kept for ninety days. The two columns are the falsifiable contract. The third column is the post-mortem framework that makes the contract legible. Building the habit in that order keeps the journal honest: if you cannot maintain the contract, the post-mortem is decorative. Once the contract is kept, the post-mortem starts paying you back in the second year, when the patterns in your own past readings (the FOMO entries that aged badly, the Fear entries that were buys in retrospect, the Euphoria entries that should have been trims) start teaching you about the investor you actually are.

What this means for your watchlist

Open a text file. Pick one position you own. Write three sentences: the claim, the kill criterion, the edge note. Date it. That is the smallest functional investment journal. Tomorrow, pick another position. By the end of the month you will have eight or ten entries, each a contract with future-you. By the end of the year you will have a record that the brain that runs your portfolio in the moment cannot rewrite. That record is the largest source of behavioural edge available to a retail investor — not because it makes you smarter, but because it stops you from being smart in the wrong direction when the stakes are highest.