The Five Emotional States Every Value Investor Should Track

Four to notice and resist, one to cultivate. The smallest taxonomy that covers the canonical traps, and what each reading actually means before the next decision is made.

Why these five emotions specifically?

Because each one maps to a documented failure mode of the value-investing process — and each is the one the canonical practitioners warn about most. Fear is the emotion behind the worst sells. FOMO is the emotion behind the worst buys. Euphoria is the emotion that suppresses kill criteria. Regret is the emotion that anchors decisions to past mistakes. Conviction is the only one of the five that the discipline asks you to build rather than resist. The five-axis taxonomy is not arbitrary; it is the smallest set that covers the canonical traps. Tracking fewer leaves a hole; tracking more dilutes the readings.

The five axes correspond to five documented decision failures in the value-investing literature: the panic sell during drawdown (Fear), the chase buy after the move (FOMO), the suppressed kill criterion during a run (Euphoria), the refusal to act after a previous mistake (Regret), and the slow accumulation of patient capital that beats the index over decades (Conviction). Each is independently observable. Each carries a different prescribed response. Conviction is the only one the framework asks you to build rather than resist, which is why it sits in its own group in the journal: the four warning signals on one side, the single anchor on the other.

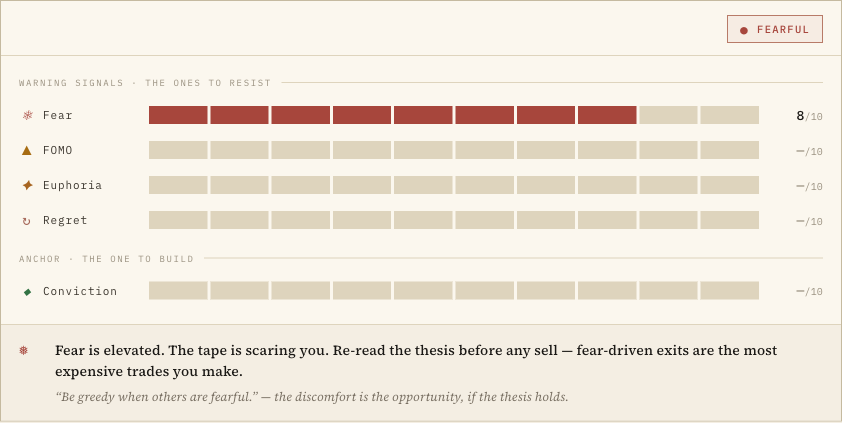

Fear · when the tape is doing the talking

The trick is to rate it before the decision, not after. A fear reading written after you have already sold reads as a justification; the same reading written before the sell reads as data. The honest test is whether you can describe the specific thing you are afraid of in one sentence. "The price is down twenty percent" is not fear; it is observation. "I am afraid the gross margin print on Tuesday will confirm the bear case" is fear, and it deserves a six or seven. Buffett's "be greedy when others are fearful" only works if you have a fear reading to react against. Without the rating, you cannot tell which side of the gradient you are on.

The classic Buffett line, be greedy when others are fearful, is only operational if you can tell when you yourself are afraid. Most fear-driven sells happen during the second half of a drawdown, when the price has been falling long enough that the bear case starts to feel inevitable. The journal entry written at that point, with the fear rating at seven or eight, is the one that future-you will re-read with relief that you did not execute the sell. The rating is the friction. Without the friction, the sell looks like prudence; with the friction, it looks like fear, which is what it usually is.

FOMO · chasing the move you already missed

It looks like reading the same earnings transcript you already read six months ago and deciding the business is suddenly more interesting because the price has moved up forty percent. The thesis has not changed. The information has not changed. What has changed is that the position has gone up, and watching it go up without you feels worse than the calculated risk of buying it now. The honest test is to imagine the same position thirty percent lower than today. Would you buy at that price? If no, you are not buying the business; you are buying the move. The FOMO rating goes to six or above the moment that test fails.

The two patterns that produce the highest FOMO readings are momentum chases and basket buys. The momentum chase is the position you would not have bought at the old price but feel compelled to buy at the new one because the move "confirms" the thesis. The basket buy is the decision to take a small position in five names from a sector that has just run, on the grounds that one of them must be a good one. Both readings should land at seven or eight; both should produce a twenty-four-hour pause. The pause is almost always the highest-return decision available — most of the names that survive the pause are no longer interesting twenty-four hours later, which is the point.

Euphoria · the only state that feels good

Because euphoria is the only one that feels good. Fear, FOMO, and regret are all uncomfortable enough that the discipline of pausing comes naturally. Euphoria is the state in which everything looks confirmed, the thesis sounds obvious, and the prudent next step looks like sizing up. Munger has called it the most dangerous of the emotional states for exactly this reason: it suppresses the discipline that other emotions trigger. A euphoria reading above six is the strongest argument the framework gives you for not adding today. The position will still be there tomorrow. The euphoria might not.

Euphoria is the one to watch on positions you already own and like. The reading spikes when an earnings print blows the doors off, when the management commentary reads like generational allocation capability, when the chart looks like the kind of thing your sceptical friends are going to ask you about at dinner. None of that is wrong; it is just the moment the discipline of the kill criteria and the trim band is most at risk of being suspended. A euphoria reading above six paired with a position above the sizing band is the exact configuration the trim policy was written for. Trim by the rule, not by the feeling. The position will be there tomorrow; the chance to act on the rule may not.

Regret · the anchor to past decisions

By rating it explicitly, which is what makes it visible. The most damaging form of regret is the silent kind: the position you trimmed too early that you now refuse to re-buy at any price, the kill criterion that fired that you now refuse to write down for the next position because the last one was "a false alarm." Writing the regret reading next to the decision creates a record: you can see, six months later, whether the regret was directional information or noise. Klarman has written that the investor's job is to make decisions that past-you and future-you would both respect. Regret is the past-you channel making itself heard; rating it is how you stop it from running the show.

Regret operates two ways. The first is the position you sold too early: the name you cannot bring yourself to re-enter at any price because that would mean acknowledging the original trim was wrong. The second is the kill criterion that fired, the one you decided was a false alarm, so you do not write one for the next position, because the last one cost you. Both forms read as conviction in the moment and reveal themselves as regret only when rated explicitly. The protection is the rating itself: the moment you write a regret reading of five or above, the framework forces you to ask whether the current decision is independently sound or whether it is being driven by the past one. Klarman's framing (make decisions past-you and future-you would both respect) is what the regret axis is testing.

Conviction · the only one to build

Conviction is the axis with the longest construction time. Fear and FOMO and euphoria can spike in an afternoon; conviction is the slow product of written thesis, kill criteria, sizing band, and the re-underwriting cadence that confirms the thesis still holds. The reading is honest at seven or eight only when the work behind it has accumulated: a name you have owned for two years, re-underwritten twice, watched through one drawdown, has earned a high conviction reading. A new name in week one of holding has not, no matter how good the analysis looks. The framework's calm-convictionsynthesis (fear, FOMO, euphoria, regret all under three, conviction at five or above) is the state the discipline is trying to produce. It is also the state in which most of the best decisions get made.

The synthesised state · Calm, Caution, Hot, Fearful

Calm in this framework is a specific synthesised state: fear under three, FOMO and euphoria each under three, regret under three, conviction at five or above. It is not zero on every axis: that reads as numb rather than calm. It is the readings of someone who has thought through the position, knows the kill criteria, knows the size, and is not currently being pushed in any direction by the tape. Conviction is the one to cultivate; the others are the ones to keep below the threshold where they start running the decision. Cultivating conviction is the slow work: written thesis, kill criteria, sizing band, re-underwriting cadence. The calm reading is the test that the work has held.

The four-state synthesis is the headline the Psychology field produces from the five axes: Fearful when fear reads six or above (re-read the thesis before any sell); Hot when FOMO or euphoria reads six or above (do not initiate or add today); Caution when any warning signal reads three to five, or conviction reads below five (act on the written policy, not on how the position feels right now); and Calm only when the warning signals are all quiet and conviction leads. The synthesis is not a verdict; it is a diagnostic. The verdict belongs to the written policy that the journal entry sits next to.

Should you ever act on these signals, or just observe them?

You observe them; you act on the written policy. The point of the rating is not to make the decision; the point is to know what state you are in before the decision is made. Fear at seven plus an unchanged thesis means re-read the thesis before any sell. FOMO at seven plus a thesis you already wrote three months ago means wait twenty-four hours. Euphoria at seven plus a position above your sizing band means trim by the written rule, not by the feeling. The rating is the diagnostic; the policy is the action. Investors who act directly on the rating are using it as a permission slip, which defeats the purpose. The discipline is in the gap between the feeling and the action.

The most useful single habit the five-axis taxonomy produces is the twenty-four-hour rule on any decision made under a Hot or Fearful reading. The decision still gets made; it just gets made a day later, after the synthesis has had time to settle and the policy has had time to assert itself over the feeling. Most decisions taken under the day-later rule look identical to what would have happened without it. The minority that do not are the ones the discipline is for — the trim that did not need to happen, the buy that did not need to be that size, the sell that did not need to fire today. The rating produces the friction; the policy produces the action; the friction is what keeps the action honest.

What this means for your next decision

Before the next entry or exit, write the five readings on a piece of paper. Fear, FOMO, Euphoria, Regret, Conviction. Each on a zero-to-ten. Do not round; do not flinch. Read the synthesis. If the synthesis is Hot or Fearful, set the decision aside for twenty-four hours and revisit the readings tomorrow. If the synthesis is Caution, open the written policy and act on it rather than on the feeling. If the synthesis is Calm, you have earned the right to execute on the work you already did. The framework does not make the decision for you; it just guarantees that the decision is being made by the version of you that the framework is willing to defend on the record.