Good capital allocation

The strategy gets the press release. What management actually does with the cash the business throws off is the decision that compounds — or quietly erodes — everything else.

Why does capital allocation matter more than almost any other management decision?

Because it compounds. Buffett put a number on it in his 1987 letter: a CEO whose company retains earnings equal to 10% of net worth each year will, after a decade, have personally decided where to deploy more than 60% of all the capital at work in the business. Strategy and operations get the attention; the decision of what to do with the cash those operations throw off is the one that actually determines whether the owner's capital compounds or leaks away.

Once they become CEOs, they face new responsibilities. They now must make capital allocation decisions, a critical job that they may have never tackled and that is not easily mastered... After ten years on the job, a CEO whose company annually retains earnings equal to 10% of net worth will have been responsible for the deployment of more than 60% of all the capital at work in the business.

Buffett wrote that in 1987, and the arithmetic hasn't aged. Skill at running the business and skill at deploying the cash the business generates are different skills, tested on different timelines, and the second one is the one most annual reports say the least about.

What is Buffett's framework for reinvest, acquire, buy back, or pay a dividend?

A hierarchy, laid out plainly in the 2012 letter. First, reinvest in the existing operations — efficiency, expansion, widening the moat. Second, look for acquisitions, ideally ones that extend what the business already does well. Third, repurchase shares, but only when they trade at a meaningful discount to conservatively calculated intrinsic value. Dividends come last — the residual, once the higher-return uses of the first three are exhausted.

The order is not arbitrary — each rung has to clear a higher bar than the one below it, because each is competing for the same dollar. Buffett's 2011 letter states the discipline that governs the bottom two rungs in particular:

The first law of capital allocation — whether the money is slated for acquisitions or share repurchases — is that what is smart at one price is dumb at another.

A buyback below intrinsic value transfers wealth to the shareholders who stay; the identical buyback above intrinsic value transfers it away from them. The action doesn't change — the price does.

What is Buffett's test for whether retained earnings were justified?

A simple, falsifiable rule from the 1983 and 1984 letters: retention is justified only if, over time, it delivers shareholders at least one dollar of market value for every dollar retained. Earnings kept inside the business are not free — they are capital the owner could have taken as a dividend and redeployed elsewhere. If retained capital compounds at less than the return available outside the business, keeping it destroyed value even though the income statement never says so.

We test the wisdom of retaining earnings by assessing whether retention, over time, delivers shareholders at least $1 of market value for each $1 retained.

The test is deliberately outcome-based rather than intention-based. A management team can narrate a reinvestment story with total sincerity and still fail the test if the ROIC on the reinvested capital never shows up in the market value. The dollar test is what turns "good capital allocation" from a character trait into something you can actually check against ten years of numbers.

What is Phil Town's ROIC test for capital allocation skill?

A numeric hurdle rather than a narrative one. Town treats return on invested capital as one of his "Big Five" numbers and sets the bar explicitly: a business needs ROIC above 10% a year, sustained over the last ten years, or it doesn't clear his bar at all. The logic runs the same direction as Buffett's dollar test — a management team can only compound outside capital's money by earning more on it than that capital could earn elsewhere — but Town's version gives you a single number to check before you read a word of the annual letter.

If a business doesn't have a healthy ROIC — above 10 percent per year on average for the last ten years — move on to another business.

Town's Management M sits inside his broader Four Ms — Meaning, Moat, Management, Margin of Safety — and the ROIC hurdle is what makes it screenable rather than anecdotal. It doesn't replace reading the letters and judging honesty and candor; it filters which letters are worth reading in the first place.

What bad capital allocation looks like

The failure mode is rarely a single bad decision — it's a pattern. Empire-building acquisitions priced to make the deal happen rather than to clear the dollar test. Buybacks that accelerate exactly when the stock is expensive, propping up EPS instead of compounding intrinsic value. Reinvestment into the existing business past the point where the incremental dollar still earns the historical ROIC — growth for its own sake, dressed up as strategy. Each looks defensible in a single year's letter. The ROIC trend and the dollar test are what catch it across ten.

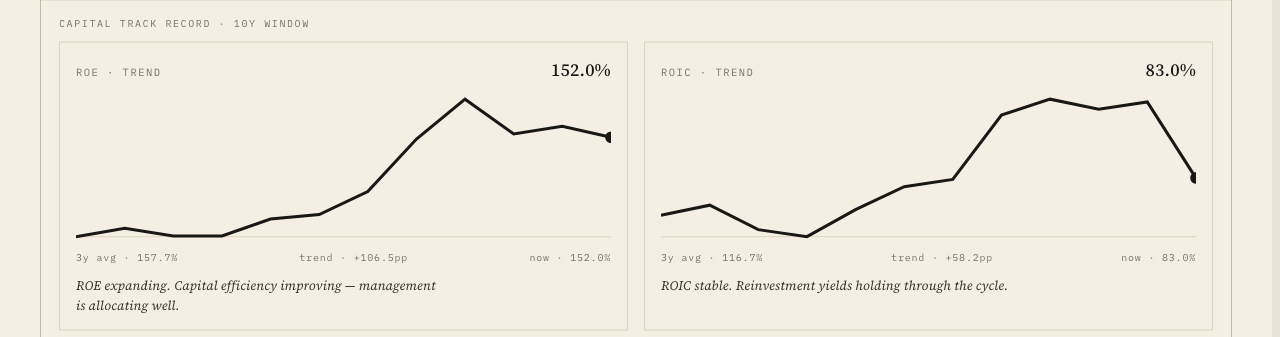

Should you look at the ROE/ROIC level, or the trend?

Both, but the trend is what actually catches deteriorating capital allocation before the letter admits it. A single year's ROE or ROIC is a snapshot; ten years of it is a report card. The practical rule: a well-run business's ROE and ROIC should hold flat or rise across a full cycle, not grind lower. A steady decline means each new dollar of retained capital is earning less than the dollar before it — which is Buffett's $1-for-$1 test failing in slow motion, well before the market value catches up to say so.

How do I check a management team’s capital allocation record on Invest Board?

The Understand tab's Management pillar scores capital-allocation skill directly, and expanding it surfaces the "Capital track record" — ROE and ROIC each plotted over the trailing decade, with a 3-year average and a trend called out in percentage points, plus a one-line read such as "ROE expanding — management is allocating well" or "ROIC compression, watch for a cyclic reset." A management team that talks about discipline but shows a falling ROE/ROIC trend has a story-versus-numbers mismatch worth reading closely before you underwrite it.